TL;DR:

- Homeowners should understand their insurance policy type to determine their out-of-pocket costs for roof replacements. Involving a licensed contractor during the claim process and filing proper supplements can significantly increase settlement amounts. Avoid small claims and out-of-state contractors to prevent premium hikes and claim denials.

The roof replacement insurance process is defined as the sequence of steps a homeowner follows to file a claim, document storm damage, work with an adjuster, and receive payment for a covered roof replacement. The average wind and hail claim totaled $14,747 between 2019 and 2023, and the full process typically runs 30 to 120 days. Massachusetts homeowners face specific challenges with this process, from nor’easter damage to insurer-specific policy terms. Understanding each stage before you file protects your payout and your premium history.

What types of coverage affect the roof replacement insurance process?

Two policy types define how much money you actually receive: Actual Cash Value (ACV) and Replacement Cost Value (RCV). ACV pays the depreciated value of your old roof. RCV pays the full cost to replace it with comparable materials. The gap between the two can easily reach several thousand dollars on a standard Massachusetts colonial.

Insurance covers sudden, accidental damage from perils like wind, hail, and fire. It does not cover gradual wear, aging shingles, or deferred maintenance. Most homeowners assume age-related deterioration qualifies. It does not, and filing a claim for it will be denied.

Massachusetts insurers often apply a depreciation schedule based on roof age. A 15-year-old asphalt shingle roof may receive a significantly reduced ACV payout even under a storm claim. Knowing your policy’s settlement type before a storm hits changes how you prepare and document damage.

Pro Tip: Pull out your declarations page right now and look for the words “Replacement Cost” or “Actual Cash Value” next to your roof coverage. That single line determines your out-of-pocket exposure.

| Coverage type | How it pays | What to watch for |

|---|---|---|

| Replacement Cost Value (RCV) | Full replacement cost, minus deductible | Final payment released only after repairs are complete |

| Actual Cash Value (ACV) | Depreciated value at time of loss | You pay the depreciation gap out of pocket |

| Covered perils | Wind, hail, fire, sudden damage | Exclusions include wear, age, and maintenance neglect |

| Code upgrade coverage | Pays for required building code upgrades | Not included in all policies; verify before filing |

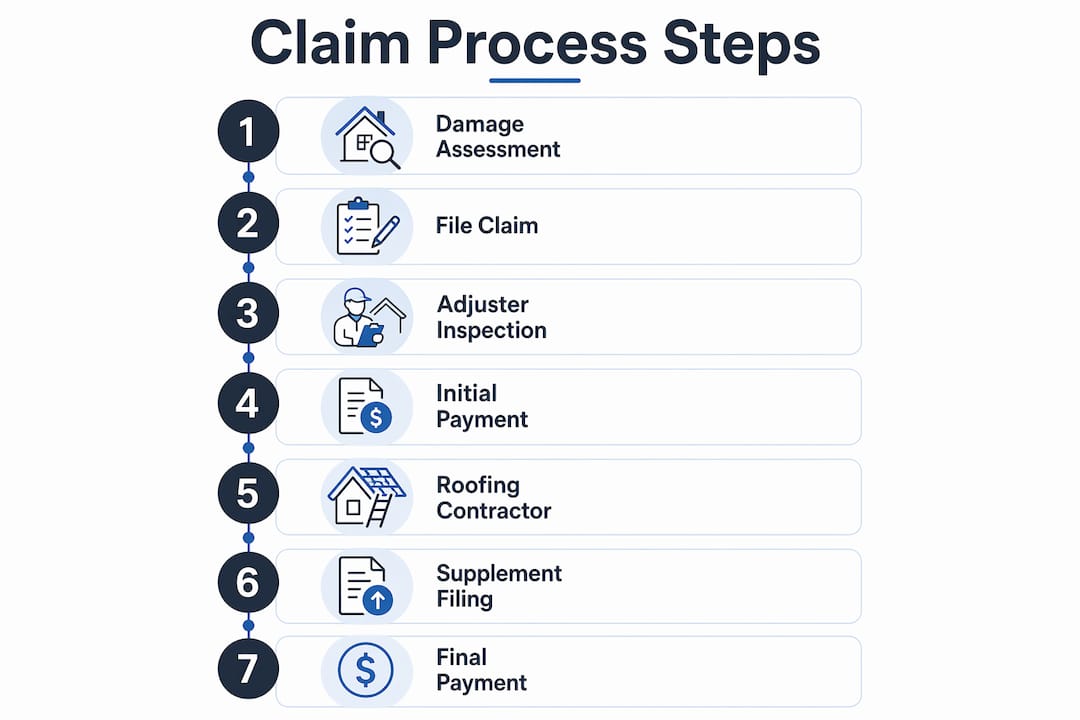

How does the roof replacement insurance claim process work step by step?

The claim process follows a clear sequence. Skipping or rushing any step costs money.

- Document the damage immediately. Take dated photos and video of every affected area, including interior water stains, damaged gutters, and missing shingles. Do this before any temporary repairs.

- File your claim with your insurer. Call or use your insurer’s app to open a claim. You will receive a claim number. Write it down and reference it in every future communication.

- Schedule the adjuster inspection. Your insurer will send an adjuster to assess the damage. This is the most important meeting in the entire process. Have a licensed contractor present.

- Review the adjuster’s estimate. The insurer will send a written scope of loss. Compare it line by line against your contractor’s estimate. Discrepancies are common and negotiable.

- File supplements for missing items. Supplements recover costs for code upgrades, drip edges, ice and water shields, and hidden damage the adjuster missed.

- Receive the initial ACV payment. Your insurer issues a first check based on the depreciated value of the roof. This is not the final payment on an RCV policy.

- Complete repairs and submit documentation. Once the roof is installed, submit the final invoice and photos. Your insurer then releases the recoverable depreciation as a second check.

The first insurance check is an ACV advance, not the total settlement. On RCV policies, the second and final payment arrives only after you submit proof of completed repairs.

Pro Tip: Never deposit the first check and assume the job is paid for. Contact your contractor and insurer the same week repairs finish to trigger the depreciation release.

Most Massachusetts homeowners see their full claim resolved within 60 to 90 days when documentation is complete and supplements are filed correctly. Delays almost always trace back to missing paperwork or an uncontested adjuster estimate.

Why does contractor involvement matter so much during the claims process?

A licensed contractor does more than install shingles. During the adjuster inspection, a contractor identifies damage the adjuster may overlook, including soft metal damage on vents, compromised flashing, and underlayment failure. Adjusters work for the insurance company. A contractor works for you.

Claims with a professional contractor present during the adjuster inspection average $18,500 to $22,000 in payouts. Homeowner-only inspections average $9,000 to $12,000. That gap reflects missed damage, incomplete scope, and no supplement filing.

The supplement process is where significant money is recovered. Properly filed supplements add an average of $7,000 per claim by recovering costs for items like code-required drip edges, ice and water shields, and damage found during tear-off. Most homeowners never know to ask for these. A contractor experienced with insurance claims files them as standard practice.

Contractors who work regularly with insurance claims also use estimating software that insurers recognize, which reduces disputes and speeds approval. Sabatalocontracting has worked with Massachusetts homeowners on storm damage claims for over 15 years, attending adjuster inspections and filing supplements as part of the standard process.

- Contractors identify soft metal damage, flashing failures, and underlayment issues adjusters routinely miss

- Supplement filing recovers code upgrade costs that adjusters do not include by default

- Contractor-prepared estimates carry more weight in insurer negotiations than homeowner-submitted photos alone

- A licensed contractor can request a re-inspection if the initial scope is incomplete

What mistakes do Massachusetts homeowners make during the insurance process?

The most costly mistake is treating the roof insurance claims process as a one-step transaction. Most homeowners who lose money do so because of avoidable errors, not bad policies.

Filing claims for minor damage near or below your deductible creates a CLUE report strike. The CLUE report is your insurance history file. Multiple claims in a short period raise your premium or trigger non-renewal. Before filing, have a contractor assess whether the damage genuinely exceeds your deductible.

- Assuming the first check is final. On RCV policies, the depreciation holdback is released only after repairs are complete and documented.

- Signing a contractor contract before claim approval. Lock in your contractor selection, but do not sign a binding contract until your insurer approves the scope and amount.

- Skipping the adjuster meeting. Homeowners who meet the adjuster alone routinely accept incomplete scopes. Always have a contractor present.

- Delaying damage documentation. Massachusetts insurers require prompt reporting. Waiting weeks after a storm weakens your claim and gives insurers grounds to question the cause.

- Ignoring supplements. Accepting the first estimate without reviewing it for missing line items leaves recoverable money on the table.

Pro Tip: Keep a dedicated folder, physical or digital, with your policy declarations page, all claim correspondence, photos, contractor estimates, and every check you receive. Disputes are won with paper trails.

How can Massachusetts homeowners maximize their insurance benefits?

Preparation before a storm determines how smoothly the claim process runs after one.

- Schedule annual roof inspections. A documented inspection history proves your roof was in good condition before the storm. Sabatalocontracting offers annual roof inspections that include written reports you can store with your policy documents.

- Install impact-resistant or fire-resistant roofing materials. Premium reductions of 5% to 35% are available for approved impact-resistant materials. Ask your insurer which products qualify before your next replacement.

- Report damage promptly. Most Massachusetts policies require reporting within a specific window after a storm. Missing that window gives the insurer grounds to reduce or deny the claim.

- Choose a licensed, local contractor. Out-of-state storm chasers disappear after payment. A local contractor with a Massachusetts license is accountable and familiar with state building codes that affect supplement claims.

- Understand your deductible type. Some Massachusetts policies carry a separate wind or hail deductible expressed as a percentage of your home’s insured value, not a flat dollar amount. A $400,000 home with a 2% wind deductible means $8,000 out of pocket before insurance pays anything.

- Review the roof replacement cost for your area. Knowing the local market rate helps you spot an undervalued adjuster estimate immediately.

Key Takeaways

The roof replacement insurance process requires documentation, contractor involvement, and a clear understanding of your ACV or RCV policy to avoid leaving thousands of dollars in unclaimed settlements.

| Point | Details |

|---|---|

| Know your policy type | ACV and RCV policies pay very differently; check your declarations page before a storm. |

| Contractor presence matters | Claims with a contractor at the adjuster inspection average nearly double the payout of homeowner-only claims. |

| Supplements recover real money | Properly filed supplements add an average of $7,000 per claim for code upgrades and hidden damage. |

| First check is not final | On RCV policies, the depreciation holdback is released only after completed repairs are documented. |

| Small claims carry risk | Filing claims below or near your deductible can raise premiums and harm your CLUE report history. |

What I’ve learned after 15 years of Massachusetts roofing claims

The adjuster inspection is the moment that determines everything. I have seen homeowners accept $9,000 settlements on roofs that warranted $21,000 simply because they met the adjuster alone and signed off on the first estimate. That gap is not a negotiation failure. It is a documentation failure.

The supplement process is the most misunderstood part of the entire claim. Homeowners think the adjuster’s estimate is the final word. It is not. Code upgrades, drip edges, and ice and water shields are required by Massachusetts building code on any full replacement, and they belong in the claim. A contractor who knows the supplement process files these as a matter of course.

My honest advice: be patient with the payment phases. The two-check system on RCV policies frustrates homeowners who expect one payment. The second check arrives after you submit the final invoice. That is the system working correctly, not the insurer stalling.

One more thing worth saying plainly: avoid out-of-state contractors who show up after major storms. They take deposits, do incomplete work, and leave. A licensed Massachusetts roofer with a local track record is your best protection against both a bad roof and a bad claim outcome.

Sabatalo contracting helps Massachusetts homeowners through every claim step

Dealing with an insurance claim while also managing a roof replacement is a lot to handle at once. Sabatalo contracting has spent over 15 years helping Massachusetts homeowners get fair settlements by attending adjuster inspections, filing supplements, and delivering quality installations that satisfy insurer documentation requirements.

From the first damage assessment to the final depreciation check, Sabatalo contracting’s licensed roofing professionals guide you through each stage. The team is familiar with Massachusetts building codes, local insurer practices, and the supplement items that most homeowners miss. Request a free inspection and estimate to get started.

FAQ

What does the roof replacement insurance process involve?

The roof replacement insurance process covers filing a claim, attending an adjuster inspection, reviewing the scope of loss, filing supplements, and receiving payment in two phases on RCV policies. The full process typically takes 30 to 120 days.

What is the difference between ACV and RCV roof coverage?

ACV pays the depreciated value of your roof at the time of loss. RCV pays the full cost to replace it with comparable materials, with the final payment released after repairs are complete.

Should I have a contractor present at the adjuster inspection?

Yes. Claims with a contractor present at the adjuster inspection average $18,500 to $22,000, compared to $9,000 to $12,000 for homeowner-only inspections, because contractors identify damage adjusters miss and file supplements for code-required items.

What is a supplement in a roofing insurance claim?

A supplement is an additional claim filed after the initial estimate to recover costs for items the adjuster did not include, such as drip edges, ice and water shields, and code upgrade requirements. Properly filed supplements recover an average of $7,000 per claim.

Can filing a small roof claim hurt my insurance?

Yes. Filing a claim for damage near or below your deductible creates a record in your CLUE insurance history report. Multiple claims in a short period can raise your premium or lead to non-renewal, so always have a contractor assess the damage before filing.

Recommended

- Massachusetts Roof Replacement: Homeowner’s Prep Guide | Sabatalo Contracting

- Storm Roofers for Massachusetts Homes: 2026 Guide | Sabatalo Contracting

- Roof Replacement Process for Massachusetts Homeowners 2025 | Sabatalo Contracting

- Roof Replacement Options for Massachusetts Homes | Sabatalo Contracting